This post, leveraging AI, summarizes and analyzes the key aspects of the research paper “Market Efficiency in Foreign Exchange Markets”. For in-depth information, please refer to the original PDF.

📄 Original PDF: Download / View Fullscreen

English Summary

{Your English summary here}

Key Technical Terms

Below are key technical terms and their explanations to help understand the core concepts of this paper. You can explore related external resources via the links next to each term.

- {Exact Technical Term 1} [Wikipedia (Ko)] [Wikipedia (En)] [나무위키] [Google Scholar] [Nature] [ScienceDirect] [PubMed]

Explanation: {Concise English explanation 1 for Term 1} - {Exact Technical Term 2} [Wikipedia (Ko)] [Wikipedia (En)] [나무위키] [Google Scholar] [Nature] [ScienceDirect] [PubMed]

Explanation: {Concise English explanation 2 for Term 2} - {Exact Technical Term 3} [Wikipedia (Ko)] [Wikipedia (En)] [나무위키] [Google Scholar] [Nature] [ScienceDirect] [PubMed]

Explanation: {Concise English explanation 3 for Term 3}

View Original Excerpt (English)

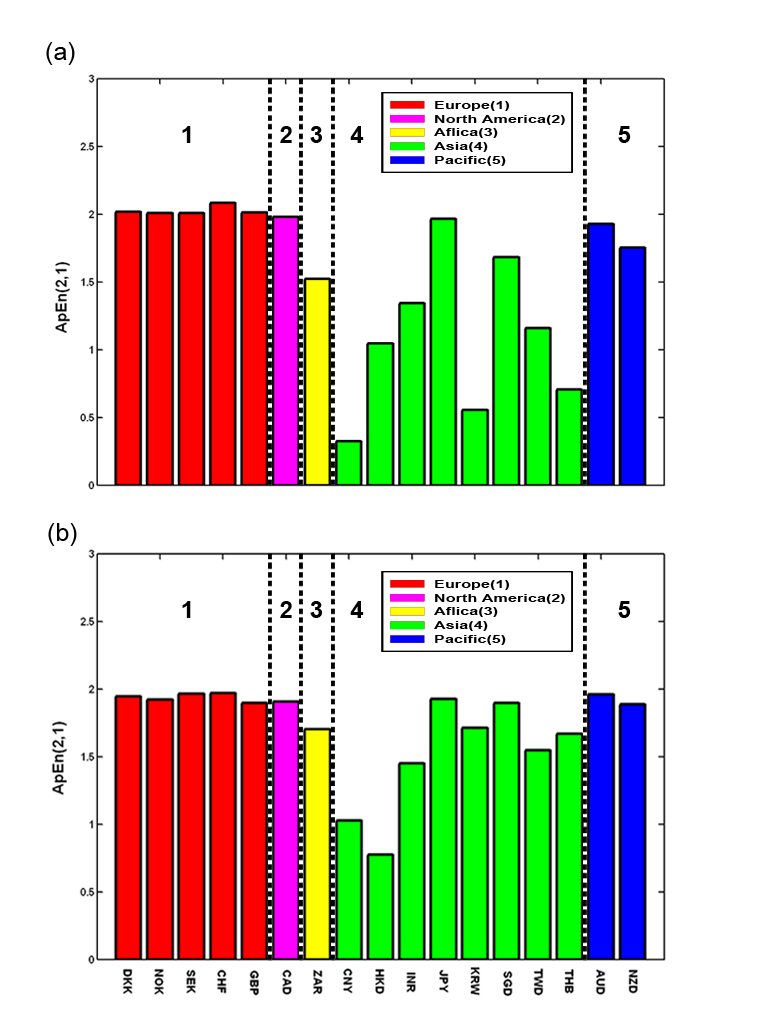

Market Efficiency in Foreign Exchange Markets Gabjin Oh∗and Seunghwan Kim† Asia Pacific Center for Theoretical Physics & NCSL, Department of Physics, Pohang University of Science and Technology, Pohang, Gyeongbuk, 790-784, Korea Cheoljun Eom‡ Division of Business Administration, Pusan National University, Busan 609-735, Korea (Received 13 11 2006) We investigate the relative market efficiency in financial market data, using the approximate2006 entropy(ApEn) method for a quantification of randomness in time series. We used the global foreign exchange market indices for 17 countries during two periods from 1984 to 1998 and from 1999 to 2004 in order to study the efficiency of various foreign exchange markets around the market crisis. We found that on average, the ApEn values for European and North American foreign exchangeNov markets are larger than those for African and Asian ones except Japan. We also found that the 15 ApEnthat theformarketsAsian marketswith a largerincreaseliquiditysignificantlysuch asafterEuropeanthe AsianandcurrencyNorth Americancrisis. Ourforeignresultsexchangesuggest markets have a higher market efficiency than those with a smaller liquidity such as the African and Asian ones except Japan. PACS numbers: 05.45.Tp, 89.65.Gh, 89.90.+n Keywords: Approximate Entropy(ApEn), Market Efficiency, Degree of Randomness I. INTRODUCTION Recently, the complex features of financial time series have been studied using a variety of methods developed in econophysics [1-2]. The analysis of extensive financial data has empirically pointed to the breakdown of the efficient[physics.soc-ph] market hypothesis(EMH), in particular, the weak-form of EMH [4-6, 12-14]. For example, the distribution function of the returns of various financial time series is found to follow a universal power law distribution with varying exponents [4-6, 13]. The returns of financial time series without apparent long-term memory are found to possess the long-term memory in absolute value series, indicating a long-term memory in the volatility of financial time series [7,8,9,11,15]. In this paper, we use a method developed in…

🇰🇷 한국어 보기 (View in Korean)

한글 요약 (Korean Summary)

{귀하의 영어 요약 여기}

주요 기술 용어 (한글 설명)

- {Exact Technical Term 1}

설명 (Korean): {1 자의 간결한 영어 설명 1}

(Original English: {Concise English explanation 1 for Term 1}) - {Exact Technical Term 2}

설명 (Korean): {2 학기의 간결한 영어 설명 2}

(Original English: {Concise English explanation 2 for Term 2}) - {Exact Technical Term 3}

설명 (Korean): {3 학기의 컨시어 영어 설명 3}

(Original English: {Concise English explanation 3 for Term 3})

발췌문 한글 번역 (Korean Translation of Excerpt)

외환 시장의 시장 효율성 Gabjin OH * 및 Seunghwan Kim † 아시아 Pacific 이론 물리학 및 NCSL, Pohang Science and Technology, Pohang, Pohang, Gyeongbuk, 790-784, Zorea CHEOLJUN EOM, PUSAN NANITIONA, BUSAN 6095, BUSAN NANITIEN 2006) 우리는 시계열에서 임의성의 정량화를위한 대략 2006 엔트로피 (APEN) 방법을 사용하여 재무 시장 데이터의 상대 시장 효율성을 조사합니다. 우리는 시장 위기에 관한 다양한 외환 시장의 효율성을 연구하기 위해 1984 년부터 1998 년까지, 1999 년부터 2004 년까지 2 개 기간 동안 17 개국의 글로벌 외환 시장 지수를 사용했습니다. 우리는 평균적으로 유럽 및 북미 외환 거래소 시장의 APEN 값이 일본을 제외한 아프리카 및 아시아 인 시장보다 크다는 것을 발견했습니다. 우리는 또한 15 개의 Apenthat theformarketsasian 시장이 더 큰 성실 성인이 asianandcurrencynorth americancrisis를 asianandcurrency를 assaftereurence로 인정하고 있음을 발견했습니다. 우리의 외계인은 대형 시장은 일본을 제외한 아프리카 및 아시아와 같은 유동성이 작은 시장보다 시장 효율성이 높습니다. PACS 번호 : 05.45.tp, 89.65.gh, 89.90.+N 키워드 : 대략적인 엔트로피 (APEN), 시장 효율성, 무작위성 정도 I. 소개 최근에, 금융 시계열의 복잡한 특징은 생태계에서 개발 된 다양한 방법을 사용하여 연구되었습니다 [1-2]. 광범위한 금융 데이터의 분석은 경험적으로 효율적인 [Physics.soc-Ph] 시장 가설 (EMH), 특히 EMH의 약한 형태 [4-6, 12-14]의 붕괴를 지적했습니다. 예를 들어, 다양한 금융 시계열의 반환의 분포 함수는 지수가 다양한 지수를 갖는 범용 전력 법칙 분포를 따르는 것으로 밝혀졌다 [4-6, 13]. 명백한 장기 메모리가없는 재정적 시계열의 반품은 절대 값 시리즈에서 장기 메모리를 갖는 것으로 밝혀졌으며, 이는 금융 시계열의 변동성에서 장기 기억을 나타냅니다 [7,8,9,11,15]. 이 백서에서는 개발 된 방법을 사용합니다.

Source: arXiv.org (or the original source of the paper)

답글 남기기